net sales totaled $2,846 million for the fourth quarter 2015, a decrease of 1.2% compared to the same period in 2014 on a constant currency basis (down 15.1% on a reported basis). EMEA net sales increased, excluding the impact of currency translation, driven by higher industry volumes and market share increases. In LATAM, net sales decreased due to the decline of the Brazilian market, partially offset by increased deliveries in Argentina. In the full year 2015, Commercial Vehicles’ net sales were $9,542 million, an increase of 4.8% compared to 2014 on a constant currency basis (down 12.4% on a reported basis) as a result of increased deliveries in EMEA. Excluding the impact of currency translation, EMEA net sales increased, driven by higher volumes, increases in market share and favorable pricing. In LATAM, net sales decreased mainly due to declining volume in the Brazilian market.

was $155 million for the fourth quarter 2015, a 55% increase compared to Q4 2014, with an operating margin of 5.4%, up 2.4 p.p. over the same period in 2014. Favorable pricing in all regions, EMEA manufacturing efficiencies and material cost reductions drove the increase in profitability. In the full year 2015, Commercial Vehicles reported an operating profit of $283 million, a $254 million increase compared to 2014, with an operating margin of 3.0% (up 2.7 p.p. over 2014), due to higher volumes in EMEA, positive pricing, manufacturing efficiencies and SG&A expense reduction as a result of the Company’s Efficiency Program. In LATAM, positive pricing, as well as manufacturing and SG&A cost containment actions, offset a large portion of the lower volumes in Brazil.

In 2015, the European truck market (GVW ≥3.5 tons) grew by 16% compared to 2014. The light vehicles market (GVW 3.5-6.0 tons) increased 16%, while the medium vehicles market (GVW 6.1-15.9 tons) and the heavy vehicles market (GVW ≥16 tons) grew by 5% and 19%, respectively. In LATAM, new truck registrations (GVW ≥3.5 tons) declined 40% compared to 2014, with a decrease of 47% in Brazil and 42% in Venezuela, while Argentina increased 5%. In APAC, new truck registrations decreased 10% compared with 2014.

The Company’s estimated market share in the European truck market (GVW ≥3.5 tons) was 11.3%, up 1.4

p.p. year over year. In the light segment, the share increased by 0.6 p.p. to 11.3%, the Company’s market share increased by 1.4 p.p. to 30.6% in the medium segment and 0.3 p.p. to 7.9% in the heavy segment. In LATAM, in 2015, the Company’s market share increased 2.4 p.p. to 12.4%.

During 2015, Commercial Vehicles delivered approximately 140,200 vehicles (including buses and specialty vehicles), representing a 9% increase from 2014. Volumes were higher in the light segment (up 13%), as a result of the launch of the new Daily, and in the heavy segment (up 9%), while volumes declined in the medium segment (down 1%). Commercial Vehicles deliveries increased 18% in EMEA, but declined 21% in LATAM and 15% in APAC.

Commercial Vehicles’ 2015 book-to-bill ratio was 1.03, an increase of 5% over 2014. In 2015, truck order intake in Europe increased 29% compared to previous year.

totaled $912 million for the fourth quarter 2015, an increase of 5.6% over the same period in 2014 on a constant currency basis (down 7.7% on a reported basis) due to positive mix on engine sales and increased volume of transmissions and axles. In the full year 2015, Powertrain’s net sales were $3,560 million, a decrease of 5.2% compared to 2014 on a constant currency basis (down 20.3% on a reported basis), primarily attributable to lower captive agricultural equipment demand, and the 2014 build-up of Tier 4 final transition engine inventory for the off-road segment. Sales to external customers accounted for 46% of total net sales in 2015 (41% in 2014).

was $62 million for the fourth quarter 2015 ($66 million in Q4 2014), at an operating margin of 6.8%. Net of the impact of currency translation, operating profit improved $5 million from favorable product mix and from SG&A expense reductions. In the full year 2015, Powertrain reported an operating profit of $186 million ($223 million in 2014), with an operating margin of 5.2% (5.0% for 2014). Net of the impact of currency translation, operating profit was in line with the previous year, as the lower volumes were offset by manufacturing efficiencies and SG&A expense reductions.

During the year, Powertrain sold 507,700 engines, a decrease of 13% compared to 2014. By major customer, 31% of engines were supplied to Commercial Vehicles, 10% to Agricultural Equipment, 4% to Construction Equipment and the remaining 55% to external customers (units sold to third parties were up 2% compared to 2014). Additionally, Powertrain delivered approximately 67,800 transmissions and 182,000 axles, an increase of 6% and 16%, respectively, compared to 2014.

Financial Services

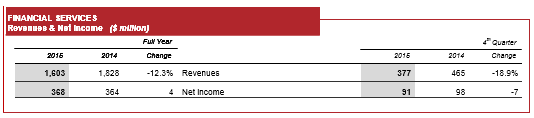

Financial Services’ revenues totaled $377 million in the fourth quarter 2015, down 8.6% compared to Q4 2014 on a constant currency basis (down 18.9% on a reported basis), due to a reduction in interest yields and lower average outstanding portfolio. In the full year 2015, Financial Services’ revenues were $1,603 million, flat compared to 2014 on a constant currency basis (down 12.3% on a reported basis).

Net income was $91 million for the fourth quarter, a $7 million decrease compared to Q4 2014, mainly due to reduced net interest margins and the negative impact of currency translation, partially offset by lower income taxes. In the full year 2015, net income was $368 million compared to $364 million in 2014. Lower provisions for credit losses and SG&A expenses, coupled with reduced income taxes, were partially offset by the impact of currency translation.

Retail loan originations in the year were $9.4 billion, down $1.4 billion compared to 2014, mostly due to the decline in Agricultural Equipment sales in NAFTA and the negative impact of currency translation in EMEA and LATAM. The managed portfolio (including unconsolidated joint ventures) of $24.7 billion (of which retail was 65% and wholesale 35%) was down $2.6 billion compared to December 31, 2014. Excluding the impact of currency translation, the managed portfolio was flat compared to 2014.

Dividends

The Board of Directors of CNH Capital N.V. intends to recommend to the Company’s shareholders at the Annual General Meeting a dividend of €0.13 per common share, totaling approximately €177 million (~$200 million). Subject to the AGM’s approval (expected on April 15, 2016), the ex-dividend date would be set at April 25, 20161.

Share Buy-Back Program

The Company today announced a buy-back program (the "Program") to repurchase up to $300 million in common shares from time to time, subject to market and business conditions, as previously authorized at the Shareholders’ Meeting held on April 15, 2015. The Program will be funded by the Company’s liquidity. Details of the Program will be disclosed in accordance with applicable laws and regulations.

2016 U.S GAAP Outlook

The agricultural equipment industry in NAFTA is forecasted to decline in 2016, with the row crop sector down 15-20%; EMEA agricultural equipment markets are expected to be flat. The commercial vehicles segment is expected to increase up to 5% in EMEA; trading conditions in LATAM are expected to remain challenging. CNH Capital is setting its 2016 guidance as follows:

•

Net sales of Industrial Activities between $23 billion and $24 billion, with an operating margin of Industrial Activities between 5.2% and 5.8%;

•

Net industrial debt at the end of 2016 between $1.5 billion and $1.8 billion.

About CNH Capital

CNH Capital N.V. (NYSE: CNHI /MI: CNHI) is a global leader in the capital goods sector with established industrial experience, a wide range of products and a worldwide presence. Each of the Company’s individual brands is a major international force in its specific industrial sector: Case IH, New Holland Agriculture and Steyr for tractors and agricultural machinery; Case and New Holland Construction for earth moving equipment; Iveco for commercial vehicles; Iveco Bus and Heuliez Bus for buses and coaches; Iveco Astra for quarry and construction vehicles; Magirus for firefighting vehicles; Iveco Defence Vehicles for defence and civil protection; and FPT Industrial for engines, transmissions and axles. More information can be found on the corporate website: www.cnhindustrial.com

Additional Information

Today, at 4:30 p.m. CET / 3:30 p.m. GMT / 10:30 a.m. EST, management will hold a conference call to present 2015 fourth quarter and full year results to financial analysts and institutional investors. The call can be followed live online at: http://bit.ly/CNH_Industrial_2015 and a recording will be available later on the Company’s website (www.cnhindustrial.com). A presentation will be made available on the CNH Capital website prior to the call.

Non-GAAP Financial Information

CNH Capital monitors its operations through the use of several non-GAAP financial measures. CNH Capital believes that these non-GAAP financial measures provide useful and relevant information regarding its results and enhance the reader’s ability to assess CNH Capital’s financial performance and financial position. They provide measures which facilitate management’s ability to identify operational trends, as well as make decisions regarding future spending, resource allocations and other operational decisions. These and similar measures are widely used in the industries in which the Company operates. These financial measures may not be comparable to other similarly titled measures used by other companies and are not intended to be substitutes for measures of financial performance and financial position prepared in accordance with U.S. GAAP and/or IFRS.

CNH Capital non-GAAP financial measures are defined as follows:

•

Operating Profit under U.S. GAAP: Operating Profit of Industrial Activities is defined as net sales less cost of goods sold, selling, general and administrative expenses and research and development expenses. Operating Profit of Financial Services is defined as

revenues, less selling, general and administrative expenses, interest expenses and certain other operating expenses.

•

Trading Profit under IFRS: Trading Profit is derived from financial information prepared in accordance with IFRS and is defined as income before restructuring, gains/(losses) on disposal of investments and other unusual items, interest expense of Industrial

Activities, income taxes, equity in income (loss) of unconsolidated subsidiaries and affiliates, non-controlling interests.

•

Operating Profit under IFRS: Operating Profit under IFRS is computed starting from Trading Profit under IFRS plus/minus restructuring costs, other income (expenses) that are unusual in the ordinary course of business (such as gains and losses on the disposal of

investments and other unusual items arising from infrequent external events or market conditions).

•

Net income (loss) before restructuring and other exceptional items: is defined as Net income (loss), less restructuring charges and exceptional items, after tax.

•

Net Debt and Net Debt of Industrial Activities (or Net Industrial Debt): CNH Capital provides the reconciliation of Net Debt to Total Debt, which is the most directly comparable measure included in the consolidated balance sheets. Due to different sources of

cash flows used for the repayment of the debt between Industrial Activities and Financial Services (by cash from operations for Industrial Activities and by collection of financing receivables for Financial Services), management separately evaluates the cash flow

performance of Industrial Activities using Net Debt of Industrial Activities.

•

Working capital: is defined as trade receivables and financing receivables related to sales, net, plus inventories, less trade payables, plus other assets (liabilities), net.

•

Constant currency: CNH Capital discusses the fluctuations in revenues and certain non-GAAP financial measures on a constant currency basis by applying the prior year exchange rates to current year’s values expressed in local currency in order to eliminate

the impact of foreign exchange rate fluctuations.

Forward-looking statements

All statements other than statements of historical fact contained in this earning release including statements regarding our: competitive strengths; business strategy; future financial position or operating results; budgets; projections with respect to revenue, income, earnings (or loss) per share, capital expenditures, dividends, capital structure or other financial items; costs; and plans and objectives of management regarding operations and products, are forward-looking statements. These statements may include terminology such as “may”, “will”, “expect”, “could”, “should”, “intend”, “estimate”, “anticipate”, “believe”, “outlook”, “continue”, “remain”, “on track”, “design”, “target”, “objective”, “goal”, “forecast”, “projection”, “prospects”, “plan”, or similar terminology. Forward-looking statements are not guarantees of future performance. Rather, they are based on current views and assumptions and involve known and unknown risks, uncertainties and other factors, many of which are outside the Company’s control and are difficult to predict. If any of these risks and uncertainties materialize or other assumptions underlying any of the forward-looking statements prove to be incorrect, the actual results or developments may differ materially from any future results or developments expressed or implied by the forward-looking statements. Factors, risks, and uncertainties that could cause actual results to differ materially from those contemplated by the forward-looking statements including, among others: the many interrelated factors that affect consumer confidence and worldwide demand for capital goods and capital goods-related products; general economic conditions in each of the Company’s markets; changes in government policies regarding banking, monetary and fiscal policies; legislation, particularly relating to capital goods-related issues such as agriculture, the environment, debt relief and subsidy program policies, trade and commerce and infrastructure development; government policies on international trade and investment, including sanctions, import quotas, capital controls and tariffs; actions of competitors in the various industries in which the Company competes; development and use of new technologies and technological difficulties; the interpretation of or adoption of new compliance requirements with respect to engine emissions, safety or other aspects of our products; production difficulties, including capacity and supply constraints and excess inventory levels; labor relations; interest rates and currency exchange rates; inflation and deflation; energy prices; prices for agricultural commodities; housing starts and other construction activity; the Company’s ability to obtain financing or to refinance existing debt; a decline in the price of used vehicles; the resolution of pending litigation and investigations on a wide range of topics, including dealer and supplier litigation, intellectual property rights disputes, product warranty and defective products claims, emissions and/or fuel economy regulatory and contractual issues; the evolution of the Company’s contractual relations with Kobelco Construction Machinery Co., Ltd. and Sumitomo (S.H.I.) Construction Machinery Co., Ltd.; the Company’s pension plans and other post-employment obligations; political and civil unrest; volatility and deterioration of capital and financial markets, including further deterioration of the Eurozone sovereign debt crisis and other similar risks and uncertainties; and the Company’s success in managing the risks involved in the foregoing. Further information concerning factors, risks, and uncertainties that could materially affect the Company’s financial results is included in our annual report on Form 20-F for the year ended December 31, 2014, prepared in accordance with U.S. GAAP and in our EU Annual Report at December 31, 2014, prepared in accordance with IFRS. Investors should refer to and consider the incorporated information on risks, factors, and uncertainties in addition to the information presented here.

Forward-looking statements speak only as of the date on which such statements are made. Furthermore, in light of ongoing difficult macroeconomic conditions, both globally and in the industries in which CNH Capital operates, it is particularly difficult to forecast results, and any estimates or forecasts of particular periods that are provided in this earnings release are uncertain. Accordingly, investors should not place undue reliance on such forward-looking statements. The Company can give no assurance that the expectations reflected in any forward-looking statements will prove to be correct. Actual results could differ materially from those anticipated in such forward-looking statements. The Company’s outlook is based upon assumptions relating to the factors described in the earnings release, which are sometimes based upon estimates and data received from third parties. Such estimates and data are often revised. The Company undertakes no obligation to update or revise publicly its outlook or forward-looking statements, whether as a result of new developments or otherwise. Further information concerning the Company and its businesses, including factors that potentially could materially affect the Company’s financial results, is included in the Company’s reports and filings with the U.S. Securities and Exchange Commission (“SEC”), the Autoriteit Financiële Markten (“AFM”) and Commissione Nazionale per le Società e la Borsa (“CONSOB”).

All future written and oral forward-looking statements by the Company or persons acting on Company’s behalf are expressly qualified in their entirety by the cautionary statements contained herein or referred to above.

Contacts

Media Inquiries

United Kingdom

Richard Gadeslli

Tel: +44 207 7660 346

Laura Overall

Tel: +44 207 7660 346

Italy

Francesco Polsinelli

Tel: +3 335 1776 091

Cristina Formica

Tel: +39 011 0062 464

Email: mediarelations@cnhind.com

www.cnhindustrial.com

Investor Relations

Federico Donati

Tel: +44 207 7660 386

Noah Weiss

Tel: +1 630 887 3745